When thinking about how to make your retirement savings last, I often ask myself: What’s the real secret to making sure money stretches as far as time? It turns out, there isn’t just one answer. It comes down to having smart, flexible strategies, not relying on outdated rules of thumb. Whether you’re near-retirement or already enjoying it, a systematic plan helps move from building your nest egg to drawing from it without risk of running dry. Let’s explore five proven methods, with examples and questions designed to help you reflect on your own situation.

“Do not save what is left after spending, but spend what is left after saving.” — Warren Buffett

Dynamic spending rules are at the heart of staying on track. Rather than withdrawing a fixed amount – say, the famous 4% rule – dynamic withdrawals work by adjusting to how your portfolio performs. If markets drop, you tighten the belt; when they soar, you can loosen a bit. Think about this: If the market tanks by 20%, would you be willing to reduce withdrawals by 10% next year to preserve capital? The flexibility here means your withdrawal plan ebbs and flows with your investment returns and avoids locking in losses during tough years. This approach offers protection against “sequence-of-returns” risk—the danger that poor market returns early in retirement could permanently reduce your eventual income.

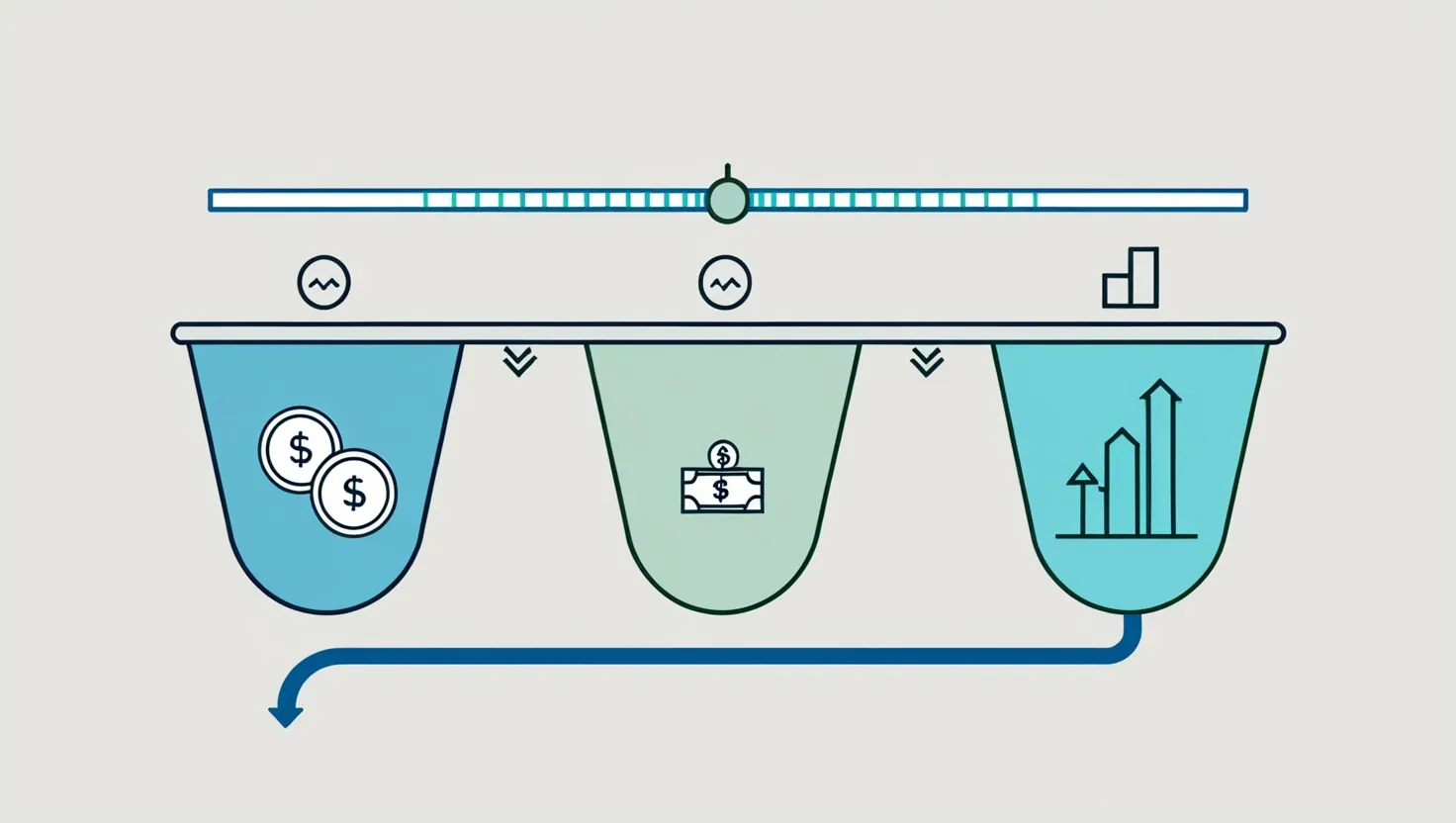

Now, what about organizing assets and withdrawals according to time? This is where the bucket strategy shines. Imagine your retirement savings divided into three parts: immediate, intermediate, and long-term needs. In practice, I might keep two years’ expenses in cash for next-to-now bills, five years’ worth in bonds or other safer investments, with the rest in stocks or growth assets for future spending. Every year, as I use cash from the first bucket, I refill it from bonds—selling growth assets only when conditions are favorable. This “time segmentation” cushions against volatility and grants peace of mind as markets move unpredictably. How comfortable would you feel knowing the next couple years’ expenses are insulated from stock market swings?

“The most powerful force in the universe is compound interest.” — Albert Einstein

Guardrail approaches take dynamic spending one step further, adding structure in the form of boundaries. Picture a system where you set upper and lower limits—for example, you never spend more than 5% nor less than 3% of your portfolio, adjusting these percentages each year depending on performance. When returns are strong, you can increase your withdrawals up to the upper “guardrail.” In down markets, you decrease them but never below your minimum living need. Periodic reviews, perhaps on each retirement anniversary, can recalibrate these boundaries—helping keep lifestyle and portfolio on track. Have you considered what level of spending feels safe during slumps, and what’s the absolute minimum you can live comfortably on?

Segmentation of essential versus discretionary expenses brings another layer of clarity. Start by covering the basics—food, shelter, healthcare—with steady, reliable income such as Social Security, pensions, or annuities. For optional expenses like travel or entertainment, use market-dependent sources like portfolio withdrawals. This dual approach helps separate needs from wants, letting you enjoy flexibility without sacrificing security. If returns are disappointing, you scale back on “wants,” but necessities remain covered. So, ask yourself: Which expenses in your budget would you prioritize, and which can be adjusted if needed?

“It is not the man who has too little, but the man who craves more, that is poor.” — Seneca

Tax-efficient withdrawal sequencing might sound technical, but it’s one of the most overlooked strategies. The order in which you draw from accounts—taxable, tax-deferred (like traditional IRAs), and tax-free (like Roth IRAs)—can make a massive difference in what you keep after taxes. Generally, experts suggest starting with taxable accounts, then moving to tax-deferred, saving Roth accounts for last. Why? Taxable accounts expose you to capital gains tax, which may be less than ordinary income tax, especially if you hold investments over a year. With Roth IRAs growing tax-free, delaying withdrawals maximizes future tax-free income. Of course, exceptions exist—higher tax bracket years, changes in legislation, or large medical expenses might shift the plan. Would you benefit from reviewing your withdrawal order with a tax advisor or experimenting with online calculators to test scenarios?

“If you fail to plan, you are planning to fail.” — Benjamin Franklin

Testing withdrawal rates against different historical market scenarios offers reality checks. I suggest using online tools to simulate how your chosen strategy would have fared in periods of both market booms and crashes. This exercise is eye-opening: a 4% rate might seem doable on average, but what happens in a decade like the 2000s or during inflation spikes? Automation, meanwhile, can simplify your life—setting up monthly transfers from designated cash buckets eliminates manual work and reduces temptation to overspend. Annual reviews are essential. Ask: How did my withdrawal rule fare last year? Has my portfolio grown or shrunk enough to merit a change?

Maintaining emergency cash outside your withdrawal system is another step the cautious rarely regret. One to two years of living expenses, set apart from both investments and regular withdrawals, insulates you from both portfolio volatility and unexpected costs—think medical bills or home repairs. It’s not just about peace of mind; it’s about practical safety.

Timing Social Security benefits, too, fits into the puzzle. Delaying benefits until age 70 can significantly boost monthly payouts, providing stronger guaranteed income to cover those essentials. This means your portfolio withdrawals can be lighter in the early years of retirement when markets might be tough, then pick up later with less risk.

Consider this: Do you know your “safe withdrawal rate,” and have you factored in your unique mix of accounts and life expectancy? Are your expenses segmented into distinguished “need” and “want” baskets? Do you know, and regularly update, the boundaries within which you’ll adjust spending? And is your plan automated, with emergency cash standing by outside the system?

“The best way to predict the future is to create it.” — Peter Drucker

In all, a systematic approach to withdrawals is not just about numbers—it’s about mindset. It gives you the ability to adapt. It’s forward-looking, realistic, and responsive to changes in markets, tax law, and personal circumstances. No system is perfect; all require review and tweaks. The best results come from coordinating these strategies: matching spending rules with the time horizon of your buckets, applying boundaries that fit your lifestyle, keeping tax efficiency at the center of decisions, and always segregating must-have from nice-to-have expenses.

For every retiree, imagination helps build resilience into the plan. Could you weather a decade of slow market growth? How would your lifestyle change if you trimmed spending during a downturn? And what is your plan for years when health or family costs spike suddenly?

The beauty of these strategies is not just their mathematical logic but their practical flexibility. With them in place, I find peace knowing retirement is not a leap into the unknown—it’s a managed transition with guardrails, buffers, and clear rules. The journey from saving to spending works best when you regularly check your assumptions, ask hard questions, and refuse to let old habits get in the way of new needs.

So, as you think about your own path, ask: Are you relying on a single “rule”—or have you built in the flexibility that life in retirement requires? Would a bucket system offer the psychological comfort you need to sleep well each night? Are your spending limits realistic and responsive, or rigid and arbitrary? And do you know how taxes and market changes might impact your plan, year by year?

Retirement isn’t a single moment. It’s an ongoing process of adjustment, review, and wise decisions—built on strategies that keep your funds intact for as long as you need them.