When I first sat down to map out my own retirement, I realized the hardest part wasn’t just growing a nest egg— it was making sure it didn’t run out. Saving is only half the battle. What really matters is how you draw down those savings, stretching them across all the years you hope to enjoy. It’s a challenge no one truly feels until they’re staring at the reality of that first withdrawal. Let’s get into some strategies that change the game for making retirement money last, with a few practical angles that might surprise you.

I’ve always been amazed how often the classic 4% rule pops up in retirement conversations. It’s simple: you start by withdrawing 4% of your portfolio in the first year and then adjust for inflation each following year. But nearly three decades after it was first introduced, the world has changed. Markets are more volatile, people are living longer, and some experts now suggest dialing that initial rate back to 3.5% (or even a touch lower) when stock valuations are high or interest rates are abnormally low. Why cling to 4% if conditions aren’t safe? I’ve found that small tweaks, like starting at 3.5% and only boosting spending in strong market years, can add a lot of peace of mind.

“Do not save what is left after spending, but spend what is left after saving.” — Warren Buffett

Still, no rule works in a vacuum. What if the market tanks right after you retire? That’s where dynamic spending shines. Rather than sticking to the same withdrawal every year, I adjust my spending up or down based on how my investments are really doing. Some years, when the portfolio dips by 20% or more, I cut withdrawals by 10% to avoid locking in losses. When my investments bounce back, I can raise them again. Is it always easy to tighten the belt? Not really. But I’d rather spend a little less in bad years than force myself back into the job market at seventy.

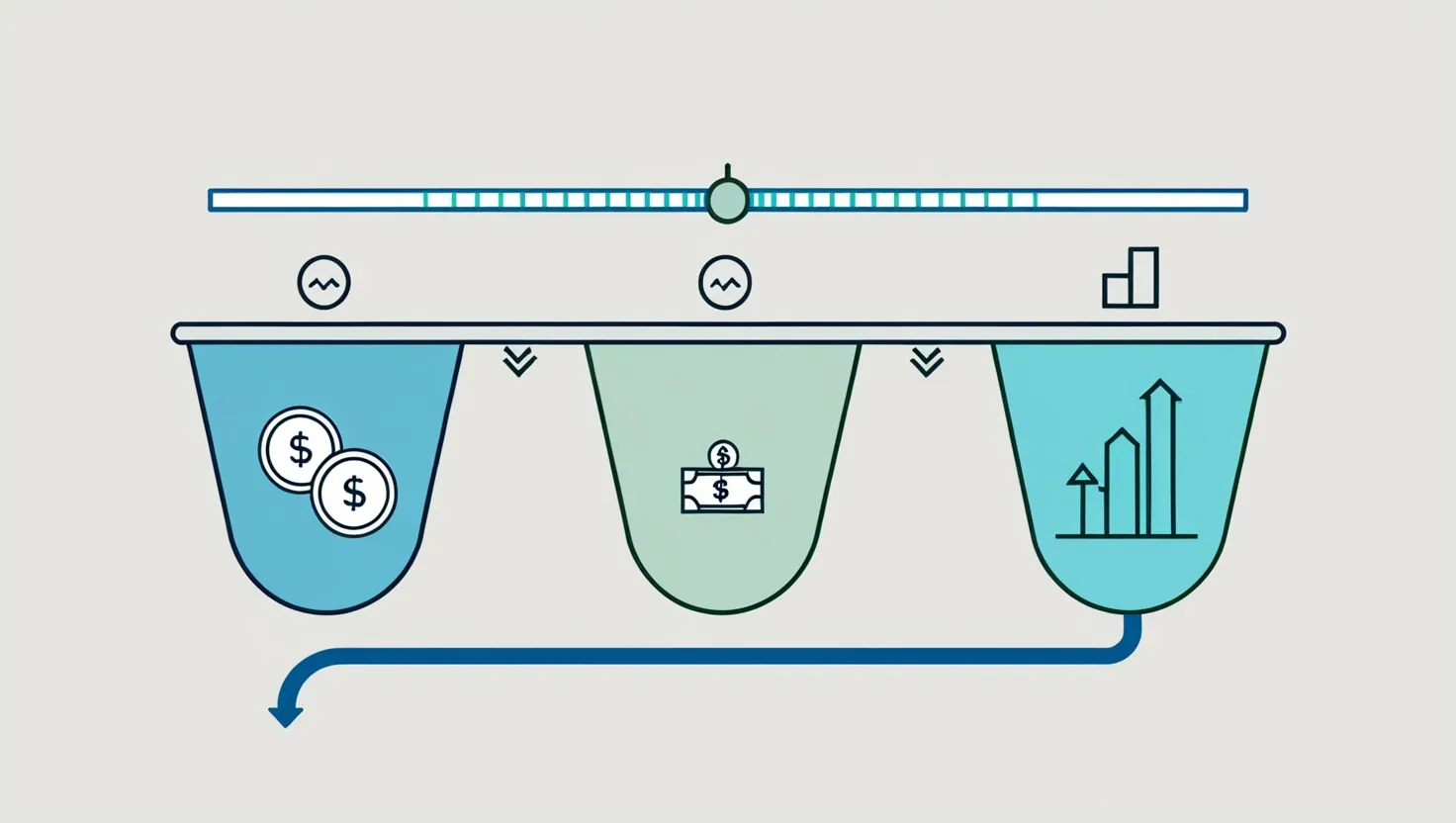

Have you ever wondered how retirees handle the anxiety of market swings? That’s where the bucket strategy steps in— one of my favorite frameworks for reducing financial stress. Here’s how it works: imagine dividing your savings into three buckets. In the first, you keep two years’ worth of expenses in cash or short-term bonds, ready for any market downturn. In the second, you put enough to cover the next eight or so years, using stable, income-producing assets. The third bucket, holding your long-term growth investments, is left alone to recover and compound. When markets dive, you dip into the safe bucket, buying time for stocks to rebound. I like how this approach translates risk into something visual— just shifting money from one bucket to another each year, rather than constantly worrying about selling at the wrong time.

I remember an advisor once asking me: “What if you could match each major expense in retirement with a guaranteed payoff, year by year?” That’s the heart of time segmentation using liability matching. It’s more precise than a simple bucket—it’s about buying bonds that mature exactly when you need cash. Suppose you know you’ll need $40,000 in year five for a new car. You buy a government bond that matures then. This way, you’re never forced to pull from stocks after a crash to pay big bills. It feels almost old-fashioned in a world obsessed with market timing, but sometimes the most boring approach can be the most reliable.

“Far more money has been lost by investors trying to anticipate corrections, than lost in the corrections themselves.” — Peter Lynch

For those who crave certainty above all, building a guaranteed income floor is deeply reassuring. This strategy focuses on meeting your essential monthly expenses—housing, food, healthcare—using predictable income like Social Security, pensions, or annuities. Everything above that can come from your investment portfolio. I’ve seen people combine immediate annuities with withdrawals from their IRAs to guarantee they’ll never go without basics, no matter what the markets do. It might not be glamorous, but it does wonders for sleep quality.

You might ask: can you mix and match these strategies? Absolutely. Some of the savviest retirees I know blend a lower initial withdrawal rate with buckets for short-term spending, precise bonds for known future needs, and annuities for their income floor. The benefit is flexibility. Life throws curveballs—unexpected healthcare bills, children needing help, sudden windfalls. Why tie yourself to just one method?

I encourage everyone to test out different strategies using free online retirement calculators. It’s easier than ever to plug in your numbers and see what each approach might look like for your own situation. Better yet, you can experiment with automatic withdrawal adjustments each year based not just on inflation, but on your portfolio’s real-world performance. Setting up annual reviews—ideally at the same time you rebalance your investments—turns this into a routine rather than an overwhelming chore.

One point that often gets overlooked is the order in which you withdraw money from different accounts. It can make a big tax difference. Generally, the most tax-efficient path involves drawing from your taxable accounts first, then from tax-deferred accounts like IRAs or 401(k)s, and finally from Roth accounts. This approach can reduce lifetime taxes, allowing your money to grow longer while you pay less to the government. Have you checked if your withdrawal order is optimized?

Most people dread the idea of reviewing their retirement plan every year, but those who do catch issues earlier and adapt more smoothly. Annual check-ins aren’t just about numbers; they’re a chance to reflect on whether your spending priorities and lifestyle have shifted. What new adventures are calling you? Have your needs or health changed? The freedom to tweak your withdrawal strategy keeps you in control, not boxed in by old plans.

“The future depends on what you do today.” — Mahatma Gandhi

As you think about retirement withdrawal strategies, remember that psychology can matter as much as math. The stress of spending down savings after a lifetime of accumulation can catch even the most prepared off guard. Building a plan that feels sustainable—one that leaves room for life’s surprises and market ups and downs—may help you enjoy retirement more fully.

Are you someone who likes to keep things simple, or do you thrive on a bit more complexity and fine-tuning? There’s no one-size-fits-all answer, just a toolkit of strategies to combine as your life and the economy evolve. As you approach retirement, challenge yourself: Which strategies feel most comfortable? Where could you add flexibility? And if you haven’t started planning your withdrawals yet, what’s stopping you?

It’s easy to get caught up in the numbers, but what really sticks with me are the stories. I’ve met retirees who spent completely differently from what they expected—taking chances on late-in-life businesses, helping grandchildren through college, or dealing with sudden health expenses. The plans that worked best were the ones that adapted, year by year, not just to the markets, but to the person’s evolving dreams and realities.

As you craft your own plan, think about what you really want your money to do for you. It’s not just about not running out; it’s about making sure you get to live on your own terms for as long as possible. And that, more than any technical strategy, is the true goal of retirement withdrawals.

“Retirement is not in my vocabulary. They aren’t going to get rid of me that way.” — Betty White

So, what withdrawal strategy are you considering? How often will you review your plan? The choices you make today can help shape a retirement that’s not just long, but meaningful and secure.